Kenneth Jeyaretnam, 1959 – 2026

Kenneth Jeyaretnam, 1959 – 2026  Another Tiger Falls in China’s Anti-Corruption Campaign

Another Tiger Falls in China’s Anti-Corruption Campaign  Swedbank fined $50 million by New York authorities over Panama Papers revelations

Swedbank fined $50 million by New York authorities over Panama Papers revelations

On any given night, thousands of people sleep on the streets in Portland, Oregon. They seek shelter in tents, bushes and overpasses in a city that has struggled with one of the worst housing crises in the country.

Portland, like many cities, has raced to increase its supply of affordable housing by turning to a federal program that’s existed since the 1980s: the Low-Income Housing Tax Credit. It provides up to $15 billion worth of tax credits a year nationally to help developers build apartments. Portland supplemented the federal construction money with local dollars, creating incentives that were hard to turn down.

But to meet the affordability requirements, all the developers needed to do in most cases was put rents within reach of someone earning 60% of median income, an earnings threshold that equates to about $75,000 annually for a family of four. It turns out that this amount of rent is now close to what the typical Portland landlord charges without any subsidy.

The result of the federal tax credit has been a glut of apartments costing renters on the order of about $1,400 a month for a one-bedroom. That’s a manageable outlay for a family making $75,000 but nearly half the monthly income of someone who earns $35,000 at the local minimum wage.

Nearly 2,000 of Portland’s subsidized units sat vacant and unused at last count, as The Oregonian and Willamette Week have reported. The same situation has repeated from Seattle to the San Francisco Bay Area to Denver.

Economists and other academic researchers have been warning for decades that this was precisely the sort of problem that the Low-Income Housing Tax Credit was likely to create.

Studies have concluded that the program, which currently supports nine out of every 10 subsidized units built in America, is an expensive and ineffective way to house people who can’t afford it. Researchers have said it doesn’t subsidize housing deeply enough to reach truly low-income renters, so it produces housing in markets and at income levels that already have a surplus instead of filling a shortage.

Independent researchers have found little evidence it’s expanded the overall housing supply beyond what the market would have produced without it. Its complexity has birthed an industry of affordable-housing-focused developers, investors, lawyers and accounting specialists who profit off the tax credit. Between 1991 and 2024, a dozen studies concluded that many more people could benefit if the money were spent on rental vouchers, which let consumers, rather than the government, decide which landlords get tax subsidies. Estimates went as high as twice the impact for the dollar.

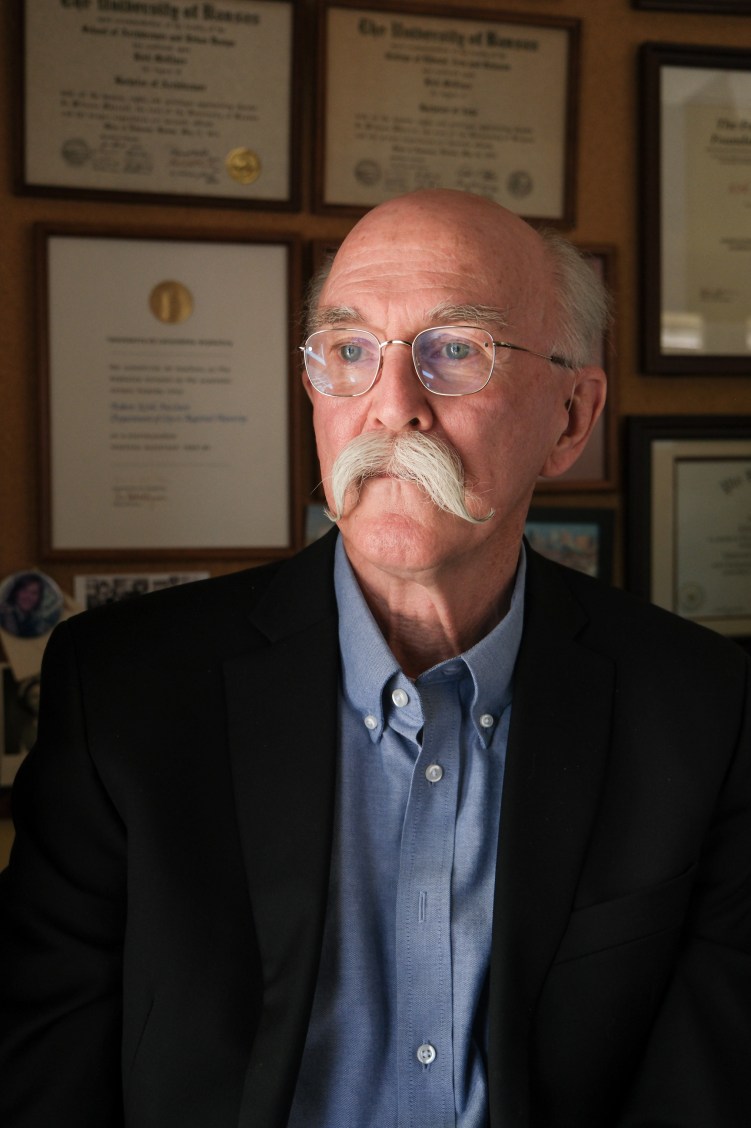

“The evidence is telling us this program is lacking its reason to exist,” said Kirk McClure, an emeritus professor of urban planning at the University of Kansas and a leading critic of the tax credit. “We should reform the program to make it work better.”

McClure and others have brought their concerns to Congress. He recommended diverting the money into rental vouchers for tenants, or else changing the tax credit’s rules to reward only developers who build units in genuinely short supply: those affordable to people at the very bottom of the income ladder.

The ideas never went anywhere. Instead, money for the tax credit has grown at a much faster rate than rental assistance vouchers since 2000, data from the U.S. Department of Housing and Urban Development and the U.S. Treasury shows. Rock-solid support from industries that benefit from the tax credit and both parties in Congress has made it the linchpin of U.S. housing policy.

“The program leverages housing market forces, entrepreneurial innovation and private accountability to increase housing supply,” former HUD Secretary Ben Carson told the House Committee on Oversight and Government Reform in 2025.

Among the tax credit’s other prominent backers are two Northwest Democrats on the Senate Committee on Finance, Ron Wyden of Oregon and Maria Cantwell of Washington. Cantwell has introduced bills to increase funding for the existing tax credit, and Wyden has proposed expanding the target of the credits to benefit not just low-income families, but also middle-income households — the opposite of what McClure says needs to happen.

Both Wyden and Cantwell say Congress should hold more hearings to ensure the program is run efficiently, but they also defended it in written statements to Oregon Public Broadcasting and ProPublica.

“There isn’t any silver bullet to the housing crisis in Oregon and around the country,” Wyden’s statement said, “but the low-income housing tax credit has been the most successful federal housing construction program on the books for decades and is the only housing program Republicans haven’t tried to gut.”

Indeed, President Donald Trump has sought to cut housing programs such as rent assistance. But as part of his spending package last year, Congress approved the biggest expansion of the Low-Income Housing Tax Credit in decades.

“That’s a mistake,” McClure said.

It won’t alleviate homelessness or the housing shortage for people at the lowest incomes, he said. It will just create more buildings that compete with the market and with one another for the same pool of renters.

McClure recounted seeing a brand-new affordable housing complex near his home in Kansas not long ago with a sign enticing tenants of another government-backed complex down the street, promoting newer units at the same price.

“So the taxpayers of the United States subsidized the creation of this new property to help bankrupt another federally subsidized property,” he said. “That is stupidity 101. We have got to be better stewards of the American taxpayer’s dollar.”

Subsidized Vacancies

Oregon’s affordable housing production has skyrocketed in recent years. So have rents and homelessness.

Over the past decade, Oregon lawmakers doubled funding for the state’s affordable housing tax credit and started offering low-interest and deferred loans for construction.

Voters in the Portland area, meanwhile, passed housing bonds totaling more than $900 million. Developers can use that money to secure federal housing tax credits. The state went from building about 1,800 affordable units a year pre-pandemic to nearly 5,000 last year.

Industries that benefit from the tax credit say it’s the engine that makes that kind of building boom possible.

The Affordable Housing Tax Credit Coalition, representing lenders, developers and others in the industry, has called the program “the most effective tool we have to meet the affordable housing needs in rural, suburban, and urban areas.”

Jennifer Schwartz, director of tax and housing advocacy for the National Council of State Housing Agencies, which advocates for the tax credit and other housing programs administered by states, said the housing market by itself won’t produce a big enough supply of housing within reach for low-income renters. That goes for even those who receive federal rent vouchers, she said.

“It costs too much to build housing to turn around and rent it to households who are low-income households,” Schwartz said, “unless you have some sort of incentive like the housing credit.”

But in Portland, all that new construction hasn’t made a dent in the city’s affordability crisis. A report from the Portland Housing Bureau in 2025 found that rent and home sale prices were growing faster than incomes, even as the city’s vacancy rate was also rising.

The vacancy rate was roughly 7.6% as of May, according to Aaron Kirk Douglas, director of market intelligence at the Portland-based brokerage HFO Investment Real Estate. Vacancies are even higher for ostensibly affordable units: 11%, leaving nearly 2,000 units unused. Housing industry experts consider 5% vacancy to be a baseline for ordinary turnover.

The time it takes to verify that a tenant’s income meets the tax credit’s requirements and prep units for move-in played a role in the struggle to fill vacant units built with the federal subsidy. But housing advocates say the biggest barrier is price.

The gap between market-rate rents and affordable housing rents has shrunk, and not just in Portland.

By one industry estimate, in more than a dozen U.S. cities at least 40% of affordable housing was competing with market-rate buildings rates in 2025.

In the Portland suburb of Gresham, federal rules cap a two-bedroom apartment built with the Low-Income Housing Tax Credit at $1,675 a month. Zillow puts the equivalent market-rate apartment at $1,525.

Operators of a new $53.8 million development in northeast Portland, built with the tax credit and the local housing bond, had trouble filling studio and one-bedroom apartments whose affordable rents were near market rate. They began offering a month of free rent for new tenants, according to a March report from the committee that oversees the region’s housing bond.

Affordable housing providers, which in Portland are predominantly nonprofit organizations, are also increasing their marketing budgets to attract renters away from market-rate buildings.

“The idea that we’re competing with the market would have been unfathomable a few years ago,” said Margaret Salazar, CEO of Reach Community Development Corporation, one of Portland’s largest affordable housing providers.

Salazar, who led Oregon’s state housing agency during the COVID-19 pandemic and later worked as a regional director for HUD, is a longtime proponent of the Low-Income Housing Tax Credit. But she said the people who can afford to rent apartments the tax credit has produced would rather move into a market-rate apartment for similar money and with fewer rules and restrictions.

“It’s becoming a slimmer and slimmer slice of residents” that Reach can serve, she said. “Suddenly we’re competing for this little slice of people.”

Meanwhile, a substantial group of Portland-area residents remain priced out.

HUD data shows more than 90,000 households in Multnomah County earn less than the 60% of median income that a family would typically need to afford a federally subsidized unit. (The precise number of families who can’t afford “affordable” units is unclear because it depends on variations in household size, actual rent levels and other subsidies that might reduce rents further.)

Salazar said that right now Reach can rent to people at lower income levels only if it can find additional subsidies such as housing vouchers — and funding for vouchers is so limited that only 1 in 4 people who qualify are able to get them.

Despite the convergence of rent levels in market-rate and subsidized housing, supporters of the tax credit say it remains valuable because the units it subsidizes are constrained from raising rents faster than incomes — and there’s no guarantee market-rate rents will remain at this level in the future.

But Steve Rudman, who ran the local housing authority in the Portland area for more than a decade, said the fact that the tax credit is now delivering market-rate housing rather than housing for the poorest households raises an existential question for the federal program.

“What is this thing really doing?” Rudman said. “What is the Low-Income Housing Tax Credit?”

A Stopgap Takes Off

Criticism of the federal construction credit has been a near constant since it began.

In the Reagan era, housing experts began to worry rents would become unaffordable amid deep cuts to housing programs and the drafting of the Tax Reform Act, which eliminated several tax shelters for real estate.

McClure, an economist for the city of Boston at the time, worked with others to design a tax credit that would reward affordable housing production.

“It was meant to be a three-year stopgap until we came up with something better,” he said.

The idea was to incorporate low-income housing into market-rate housing construction that was already taking place. Developers could receive a tax credit if they capped rents for a certain portion of the apartments in their building, and they could continue to rent the rest at any amount they chose.

McClure crafted letters for Boston’s mayor to send Congress in support of the idea. His analysis helped decide the subsidy amount. Developers could offset 70% of the cost of new builds or 30% of the cost of a rehab. Congress signed off in 1986.

Almost immediately, the program diverged from the outcomes McClure had envisioned.

He and other drafters of the tax credit had thought developers would use it to offer deep discounts on a small number of units, allowing them to charge market rate on the rest. But developers found it more profitable to subsidize 100% of their units at the smallest allowable discount, a rent affordable to households at 60% of median income.

In 1992, as lawmakers considered making the 6-year-old Low-Income Housing Tax Credit permanent, an analysis by the Congressional Budget Office declared the program “unlikely to substantially increase the supply of affordable housing” and “more suited to the needs of investors than poor renters.”

For one, the tax credits cost a lot to administer, congressional economists said. They also pointed to evidence that subsidized housing production dampened market-rate construction.

Congress was preparing to give developers $3 billion through the tax credit as of 1992. Putting that money into housing vouchers instead, the CBO concluded, would help 550,000 households, more than twice as many as would benefit from the construction tax credit. The numbers echoed findings from an earlier HUD evaluation of tax credits vs. vouchers.

Congress made the tax credit permanent a year later.

As time wore on, McClure’s emerging doubts about a program he originally expected to be temporary only deepened.

When the Fannie Mae Foundation hired him in 1997 to analyze how the tax credit was doing, he concluded it was a “very inefficient subsidy delivery mechanism” that didn’t produce as much housing as it should have.

Other studies came to similar conclusions as McClure, HUD and the Congressional Budget Office. At least five found the tax credit does little to increase the overall housing supply.

The Government Accountability Office noted problems with the program in 2015, 2016, 2017 and 2018, finding it lacked basic oversight to show the federal funds worked as intended. A 2017 investigation by NPR and Frontline documented numerous examples of waste and fraud, including one developer pocketing tax credits without building the required housing.

“Given the available evidence on program performance, we should certainly not expand the tax credit program,” Edgar Olsen, professor emeritus of economics at the University of Virginia, wrote in a 2017 article for the American Enterprise Institute. “The existing evidence argues for terminating it.”

There are some critics within Congress. Rep. Glenn Grothman, a Republican from Wisconsin, introduced a bill to kill the program last year, calling it a “cash grab for developers and banks.” But the bill went nowhere.

Olsen, like McClure, remains adamant today about what he considers the tax program’s uselessness. In a recent interview, he told OPB and ProPublica that he’s urged policymakers, in academic articles and in testimony, to re-examine whether the program has any value at all.

“How often do they talk to people like me or like Kirk McClure? The answer is almost never,” Olsen said. “What they hear from are people who represent the financial interest of the industry, and so they want more money to be spent on this.”

Don't Miss:

-

On This Nearly Deserted Alaska Island, You Pay to Keep Hundreds of Empty Buildings Wired for Internet

-

Children in This Church Were Sexually Abused. Then They Began Abusing Other Kids. Some Continued as Adults.

-

Trump Officials Want to Use Human Rights Aid to Advocate for White South Africans and Right-Wing Causes in Europe

-

How a Man Once Ordered to Pay Libel Damages Helped Launch an Investigation Into Islamic Private Schools

-

How a Paid Expert Reversed His View of a Notoriously Flawed Prosecution in the Rape of a Bestselling Author